Ira Singh

Ira Singh

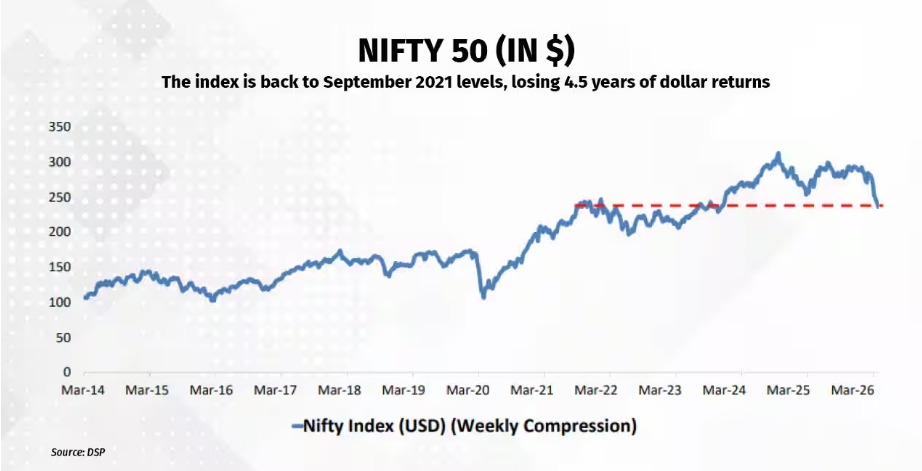

India’s benchmark equity index, the Nifty 50, has delivered virtually no returns in dollar terms since September 2021, highlighting the impact of currency depreciation and sustained foreign investor outflows on market performance.While headline gains in rupee terms have appeared modest over the past 18 months, the picture looks far less encouraging when adjusted for the weakening Indian rupee. The currency’s sharp decline falling nearly 11% in FY2025–26, its steepest drop since FY2011–12 has effectively erased gains for global investors, pushing the dollar-adjusted index back to levels seen over four years ago.

Investor sentiment has also been dented by persistent selling from foreign institutional investors. In March alone, FPIs offloaded a record Rs1.2 lakh crore worth of equities, reflecting a broader shift towards safer global assets amid rising geopolitical uncertainties. India’s status as a net energy importer has further compounded concerns, with elevated crude oil prices due to tensions in West Asia weighing on macroeconomic stability and fiscal calculations.

According to a recent report by DSP Asset Managers, India’s capital account has slipped into deficit, driven by weak foreign direct investment inflows, continued FPI outflows, and rising outward investments by domestic players. The report also flagged stretched valuations and a fragile macroeconomic backdrop as key headwinds.

Echoing similar concerns, Nithin Kamath noted that foreign investor interest in India has waned significantly. He pointed to geopolitical risks, high valuations, lack of strong artificial intelligence-led investment opportunities, and tax-related frictions as factors reducing India’s attractiveness relative to other markets. He added that reforms in capital gains taxation and securities transaction tax could help revive foreign inflows.Despite the sustained pressure, market indicators suggest a potential turning point. The DSP report highlighted that the Nifty’s relative strength index (RSI) has entered oversold territory—its lowest since the market crash during the COVID-19 pandemic—which historically has preceded phases of recovery.

Analysts believe that while current conditions remain challenging, improving valuations could eventually attract long-term capital. Historically, significant foreign inflows into Indian markets have occurred during periods of subdued sentiment rather than peak optimism, raising hopes that the current phase may lay the groundwork for a future rebound.

(Business Correspondent)

Related Items

The unpaid internship Is breaking India’s middle-class promise

India and Mongolia are strategic partners, spiritual siblings: Jaishankar

Pakistan threatens India over Indus Waters Treaty